Can You Buy a House in the U.S. Today? Yes—Here’s What You Need and Your Options

Posted on 04/18/26 at 14:43

The US housing market picked up momentum again in March, even as mortgage rates continue to rise.

For first-time homebuyers, this creates a window of opportunity—but also introduces new challenges in costs and financing.

- Why it matters: Although more homes are available, the monthly cost of buying continues to increase. Understanding how the market works and taking advantage of government programs can make the difference between buying a home or being priced out.

The US Housing Market Rebounds Despite Higher Rates

The latest report from Zillow shows that 281,546 properties were pending sale in March—the second-highest figure for any month since August 2022.

Additionally:

- New sales increased 4.6% year-over-year and 29.8% month-over-month, the largest March increase since 2021.

- Housing inventory has risen for 28 consecutive months.

- Views of home listings were 32% higher than last year.

This suggests that despite tighter financial conditions, housing demand remains strong. According to Zillow, this is partly due to pent-up demand after years of low activity and the start of the peak buying season.

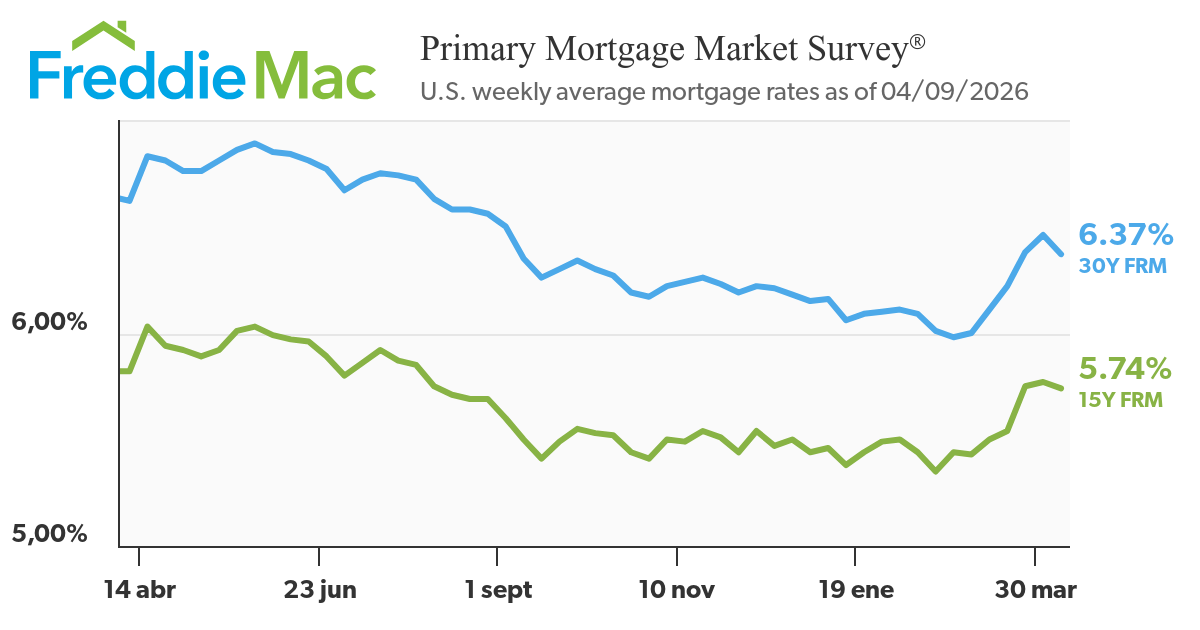

Mortgage Rates Rise and Increase Buying Costs

One of the main obstacles remains financing. According to Freddie Mac, mortgage rates rose from 5.98% at the end of February to 6.38% by the end of March.

This increase had a direct impact:

- The typical mortgage payment rose 1.5% in just one month

- The affordability gains seen earlier in the year diminished

This is compounded by uncertainty around energy costs and other economic factors that have affected buyers since the pandemic.

Government Programs That Can Help You Buy a Home

In this context, federal and state programs are key to improving access to homeownership in the US housing market in 2026.

- FHA Loans (Federal Housing Administration):

These loans allow buyers to purchase a home with a down payment as low as 3.5%, provided they meet certain credit requirements. The government does not lend directly but insures the loan, making approval easier. - VA Loans (Department of Veterans Affairs):

Designed for eligible military members and veterans. These loans offer 0% down payment and no monthly mortgage insurance, significantly reducing costs. - USDA Loans (Department of Agriculture):

Aimed at rural and suburban areas. They also allow 0% down payment, provided income and location requirements are met. - Down Payment Assistance (DPA):

State or local programs that can cover part or all of the down payment. Some are grants, while others are loans with favorable terms.

Recent Changes Could Lower Monthly Mortgage Payments

The Federal Housing Finance Agency announced new rules for loans backed by Fannie Mae and Freddie Mac that eliminate certain home insurance requirements.

According to the agency, this could lead to lower insurance premiums and, therefore, reduced monthly payments for millions of buyers—especially in rural areas and multifamily buildings.

You may also like: New York rent surpasses $4,000 and salaries fall short: what happened to Mamdani’s plan?

What’s Ahead for Buyers in 2026

The housing market shows signs of activity, but it remains challenging. There are more options available, but also increased pressure on monthly costs.

For those looking to buy:

- Understanding the market is essential

- Taking advantage of assistance programs can reduce upfront costs

- Preparing for closing costs remains crucial

In this environment, those who combine clear information with a solid financial strategy have a better chance of achieving homeownership—even with higher interest rates.